![]() As we approach 2025, corporate sustainability continues to evolve into a standard component of any business. In this article, we suggest five things that business leaders and sustainability teams should look for in 2025.

As we approach 2025, corporate sustainability continues to evolve into a standard component of any business. In this article, we suggest five things that business leaders and sustainability teams should look for in 2025.

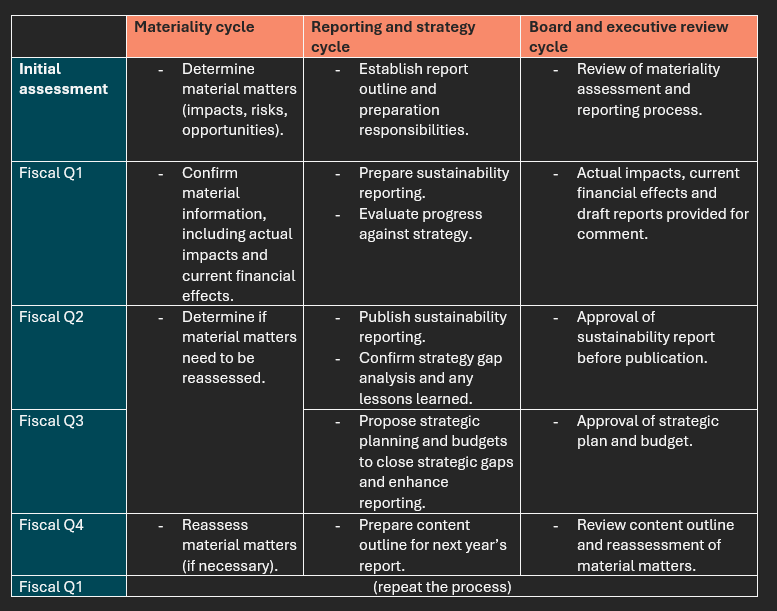

The annual cycle of materiality-strategy-reporting will become commonplace

To maximize the strategic value of sustainability reporting, companies should integrate their materiality assessments and reporting processes into their corporate strategy and budgeting cycles.

The below table explains how the annual cycle of materiality can be integrated into strategic planning.

Read more here.

Materiality will pivot from material 'matters' to material 'information'

In the era of mandatory sustainability reporting, companies must sharpen their ability to distinguish between material matters and material information. Material matters are the significant sustainability topics relevant to a company, such as health and safety or greenhouse gas emissions. Unlike materiality assessments of old, however, identifying these matters is only the first step.

The critical skill for 2025 will be determining the specific information within these matters that is material for report users. This process is crucial, as it protects against reporters omitting information because it is unfavorable rather than immaterial. Such an omission may now become a material misstatement, potentially leading to allegations of fraud or management bias.

Read more here.

Sustainability reporting teams will find their footing with finance

A common misconception is that financially material information must be identical across financial statements and sustainability reporting. Both the European Financial Reporting Advisory Group (EFRAG) and the IFRS Foundation have refuted this idea.

Companies must develop the ability to make distinct materiality judgments for sustainability disclosures. It is expected that material information for sustainability reporting might not be material for financial statements, and vice versa. This requires a repeatable and documented process for determining material information as well as a robust collaboration between sustainability and finance teams.

Read more here.

Companies acknowledging value chain impacts and experimenting with estimation

An objective of sustainability reporting is to better account for issues across a company’s value chain. Although a company may want to avoid acknowledging negative impacts in their value chains, omitting a material impact because it is too difficult to report on runs the risk of being flagged as management bias or fraud during assurance.

While the standards are firm on including value chain impacts in the materiality assessment, they understand that getting data on value chain impacts is a challenge. They allow companies to estimate impacts using sector averages and proxies – estimating scope 3 emissions using spend data is an example. Expect to see more companies experimenting with estimations on a wider range of value chain impacts.

Read more here.

We will finally recognize that we can’t fit it all into a single sustainability report

Companies produce a range of financial reports – annual reports, proxy statements, investor presentations, and so on. Companies would balk at the idea of combining all of this into a single report.

Yet many companies still contemplate how to meet their sustainability reporting requirements in a single document. For multinationals subject to a range of country-level reporting requirements, fitting everything into a single report is not only challenging, but also runs the risk of the regulator claiming that the report obscures material information.

As reporting requirements evolve, companies may realize that producing a suite of sustainability reports is the most effective way to meet the array of requirements they face.

Read more here.

Alex Gold

Dr Alex Gold is the CEO of BWD North America. He has worked across two continents as a consummate sustainability professional, having honed his strategy and reporting capabilities in senior management roles at large public companies. He is an expert...